Owning a home is a goal that many people dream of. However, when a house purchase is made with a mortgage loan, the owner must make monthly payments to the lender. If those payments stop due to financial trouble or any other reason, the lender has the legal right to take the house back and sell it to recover the unpaid loan amount. This legal process is called foreclosure. Foreclosure is not something that happens overnight, and it usually follows a step-by-step procedure that gives the homeowner warnings and chances to correct the situation before losing their home.

Foreclosure is one of the most unfortunate financial experiences a household can face. It affects not only the financial future of the borrower but also their housing security. To understand foreclosure properly, we need to look at what leads to it, how the process works, and what the long-term consequences can be.

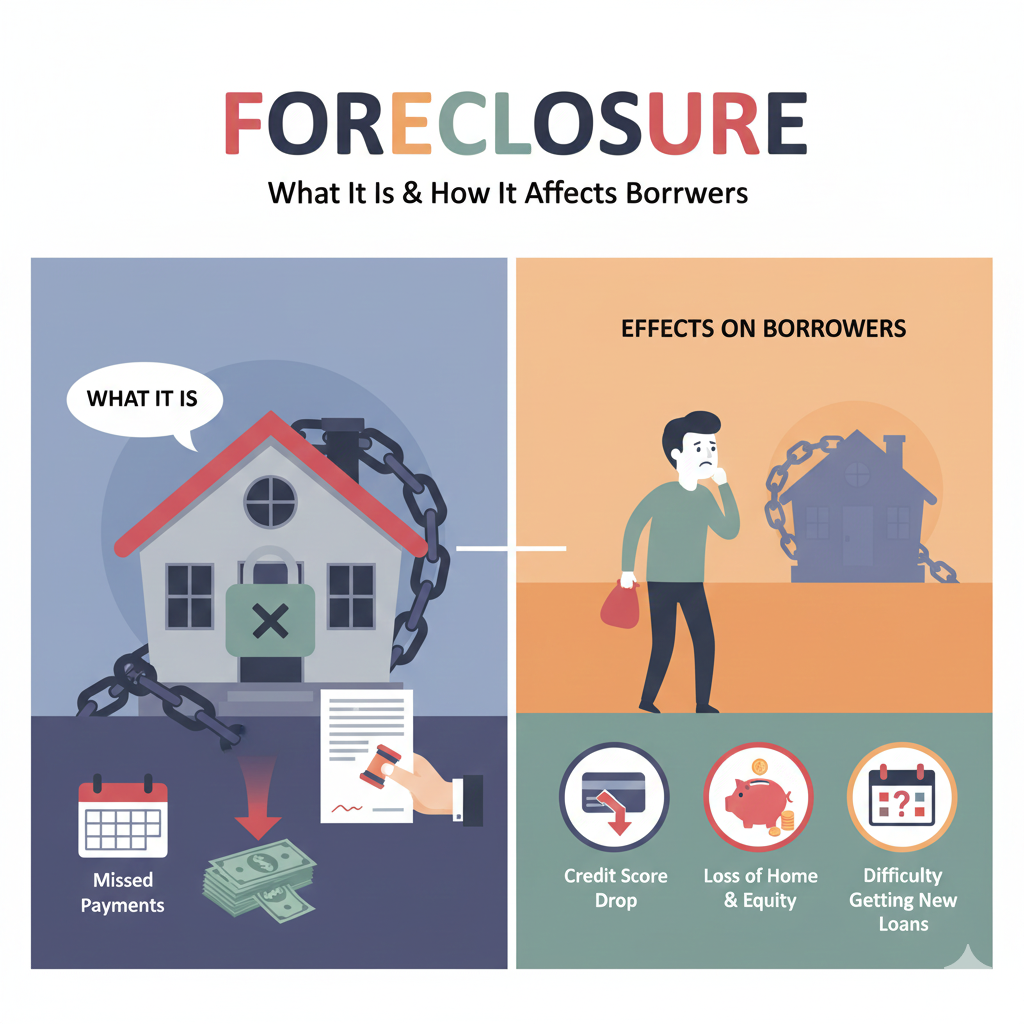

What exactly is foreclosure?

Foreclosure happens when a borrower fails to make their mortgage payments as agreed. When someone takes a home loan, they promise to repay it every month. The property itself becomes a security for that loan, meaning the lender has the right to take the property back if the borrower fails to pay.

So, foreclosure means the lender seizing the property and selling it. The sale amount is then used to pay the remaining loan balance, fees, and legal charges. If any extra money remains after everything is paid, it may go back to the borrower, though this rarely happens.

When does foreclosure start?

Foreclosure usually begins after several missed monthly payments. Many mortgage contracts allow up to three missed payments before a formal foreclosure notice is issued, but the exact rule depends on the agreement and state law.

In some cases, foreclosure may also occur if a borrower breaks another term of the mortgage agreement, such as failing to maintain insurance on the property or committing fraud. However, the most common reason is simply missing the required payments.

Foreclosure is a step-by-step legal process

Foreclosure has stages, and these stages generally look similar across most states, although exact rules vary. The stages often include:

1. Payment default

The borrower stops making payments for a certain number of months. The lender first sends reminders, late notices, and warnings.

2. Notice of default

If payments are not resumed, the lender issues a formal legal notice that foreclosure action may start.

3. Notice of sale

If the situation still does not improve, the lender publishes a notice that the property will be sold publicly.

4. Auction

The property is then listed for sale at a public auction. Interested buyers bid, and the highest bidder usually gets the property.

5. Bank ownership

If nobody buys the property during auction, the lender takes ownership. In this case, it becomes what is called a “bank-owned” or “REO” (Real Estate Owned) property.

6. Eviction

Once ownership legally transfers, the former homeowner may be asked to leave. If they do not leave voluntarily, forced eviction can occur.

Judicial vs Non-Judicial foreclosure

Different states in the United States have different foreclosure systems. Some states follow judicial foreclosure, while others allow non-judicial foreclosure depending on the mortgage contract.

Judicial foreclosure

In this method, the process must go through the court system. A judge reviews the case and authorizes the foreclosure. Because it requires legal proceedings, it usually takes longer and offers more time and chance to fight foreclosure legally.

Non-judicial foreclosure

In this type, the mortgage agreement already contains a “power of sale” clause, which gives the lender permission to sell the house without involving the court. It usually happens faster than judicial foreclosure.

What happens to the property after foreclosure?

Once the foreclosure is completed, the property goes up for sale. At an auction, potential buyers try to purchase the property. But if nobody is interested or the lender’s requirements are not met, the bank takes ownership. After that, the bank may list the house for sale on the regular real-estate market and try to recover the loan amount by selling it.

Properties that go through foreclosure often get labeled “bank-owned,” “foreclosed property,” or “REO property” on real-estate listings.

Impact on the homeowner

Foreclosure is a very serious outcome for the homeowner. The most immediate consequence is the loss of the home itself, but the effects go far beyond that. Losing a home can make it harder to find new housing, especially if the person has a damaged credit profile.

The major consequences include:

- losing the house permanently

- possible eviction from the property

- a major drop in credit score

- difficulty getting another mortgage

- higher interest rates in future borrowing

Foreclosure stays on a credit report for years, which affects future loan approvals, rental agreements, and sometimes even employment background checks.

Why foreclosure hurts credit

A foreclosure signals to lenders that the borrower failed to manage an important financial responsibility. Because a mortgage is a long-term commitment, banks take foreclosure very seriously. It shows that the borrower defaulted on a large debt, and therefore might be risky to lend money to again.

This is why getting another mortgage later becomes difficult and interest rates tend to be higher when approved.

Is foreclosure avoidable?

Foreclosure often comes at the end of a long period of financial trouble. However, there are ways to prevent foreclosure, such as mortgage refinancing, loan modification, or negotiating payment options with the lender. Many lenders prefer finding a solution rather than going through the complicated, lengthy foreclosure process.

Foreclosure is hard but not impossible to recover from

Even though foreclosure creates serious challenges, it doesn’t mean a person can never become a homeowner again. With responsible financial behavior and rebuilding credit, many people eventually buy another home after some years.

Final Thought

Foreclosure is a legal and financial process that comes into play when a borrower fails to pay their mortgage. It results in the lender taking possession of the house and selling it to recover their money. The process includes warnings, notices, and legal steps, and its consequences can be long-lasting. Foreclosure harms credit, causes loss of property, and may lead to eviction—and it takes years to fully recover financially.

Still, foreclosure is not always the end of financial life. People can rebuild, repair credit, and start again. But ideally, foreclosure should be prevented early by communicating with lenders and seeking alternatives before payments stop.