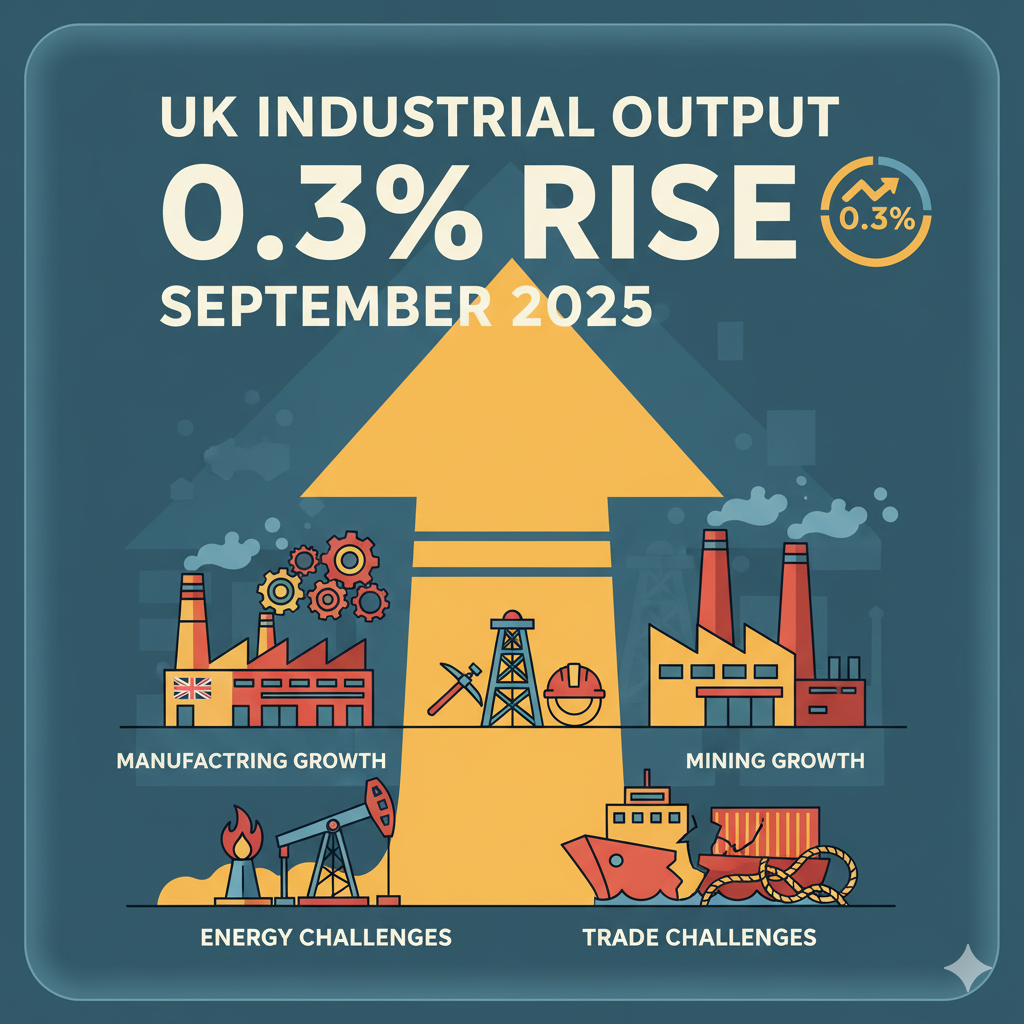

The United Kingdom’s industrial sector posted a moderate yet encouraging improvement in September 2025, signaling resilience amid a complex global economic landscape. According to the latest data from the Office for National Statistics (ONS), the Index of Production (IoP) recorded a 0.3% month-on-month increase, underscoring steady progress in the country’s key production sectors.

While the gains may appear modest at first glance, the data marks a continuation of the UK’s gradual industrial recovery following a challenging year shaped by supply chain disruptions, fluctuating energy costs, and uncertain export demand. The 1.4% year-on-year rise in total production further reinforces optimism that the UK’s manufacturing and industrial bases are stabilizing.

Manufacturing Leads the Way

The standout performer in the latest IoP report was the manufacturing sector, which rose by 0.4% in September 2025. This growth was primarily driven by strength in transport equipment manufacturing, reflecting robust demand for vehicles and parts as both domestic and international orders picked up.

Additionally, chemical production showed a healthy rebound, buoyed by improvements in raw material availability and a gradual normalization of input costs. This resurgence in manufacturing output suggests that earlier concerns about energy price pressures and weak global demand may be easing, at least in the short term.

Manufacturing remains a cornerstone of the UK economy, accounting for around 10% of GDP and providing essential export revenue. The sector’s consistent improvement offers a measure of stability to an otherwise mixed economic outlook, especially as service industries and construction continue to face varied levels of performance.

Energy Production Faces Headwinds

Despite the positive movement in manufacturing, energy production was a drag on overall industrial growth during September. The ONS reported a decline in electricity and gas output, primarily due to lower seasonal demand and shifts in energy sourcing patterns.

The UK’s energy industry has undergone significant changes in recent years, particularly with the transition toward renewable sources and reduced reliance on fossil fuels. While this structural shift supports long-term sustainability goals, it has introduced short-term volatility in production data.

Energy firms have also been navigating global commodity price fluctuations and regulatory changes tied to the UK’s decarbonization targets. These factors contributed to the subdued performance within the energy sector during September, slightly offsetting gains made elsewhere in the industrial landscape.

Mining and Quarrying Add Support

In contrast, the mining and quarrying sectors registered a moderate increase in output, offering additional support to the IoP. The growth was attributed to stable oil and gas extraction activities, which remained resilient despite external market challenges.

Steady extraction rates and improved maintenance efficiency in offshore operations helped maintain consistent production levels. While this sector is smaller compared to manufacturing, its contribution to industrial stability remains important, especially given the role of energy commodities in the UK’s broader economic balance.

The performance of mining and quarrying also underscores the gradual normalization of global commodity markets after several years of volatility. This steady footing could provide a buffer for the UK industrial base as it continues to adapt to post-pandemic economic realities.

Industrial Stability Amid Broader Economic Challenges

Analysts have interpreted the September 2025 figures as a sign of industrial stability, noting that consistent monthly gains, even if modest, represent progress in an otherwise uncertain environment.

The UK’s industrial sector continues to face multiple headwinds, including soft export demand in the European Union, persistent supply chain frictions, and fluctuating input prices. However, the ability of core sectors like manufacturing and mining to maintain growth highlights their resilience and adaptability.

Several economists suggest that industrial production could remain on a positive path if global trade conditions improve and energy prices remain stable through the winter. Continued fiscal discipline and targeted government incentives for domestic manufacturing could also enhance long-term growth prospects.

Policy Support and Market Implications

The Bank of England (BoE) has kept a close watch on industrial data, viewing it as a key indicator of underlying economic momentum. A consistent rise in the IoP aligns with the central bank’s objective of ensuring steady, sustainable growth amid a cautious monetary environment.

With inflation showing gradual moderation in late 2025, the BoE’s current policy stance may allow for a balanced approach to managing growth without reigniting price pressures. The industrial sector’s recovery could therefore contribute to a more optimistic outlook for the UK’s fourth-quarter performance.

Financial markets have also reacted positively to the latest production figures. The pound sterling remained stable following the release, while equity investors expressed confidence in sectors tied to manufacturing, logistics, and energy infrastructure. This sentiment suggests a gradual improvement in investor perception of the UK’s industrial prospects.

Export Trends and Global Linkages

The UK’s export-oriented manufacturers have benefited from a combination of improving global demand and a relatively competitive exchange rate. Demand from non-EU trading partners, particularly the United States and parts of Asia, has helped offset weaker orders from Europe.

However, businesses continue to cite customs delays and regulatory frictions as barriers to smoother trade flows. The ongoing need for clarity around trade policies and international standards remains a priority for sustaining growth in export-driven industries.

The government’s continued push for new trade agreements and partnerships aims to diversify export markets, reducing dependency on a few key regions. If successful, such diversification could reinforce industrial output and shield the UK from external shocks.

Outlook for the Remainder of 2025

Looking ahead, most analysts anticipate that industrial production will maintain modest growth through the remainder of 2025, supported by improving supply chains, stable energy conditions, and policy alignment.

However, the pace of recovery is expected to be gradual rather than rapid. A sustained uptick in industrial activity will likely depend on factors such as global economic stability, domestic demand, and continued progress in digital transformation across production facilities.

In the longer term, the UK government’s emphasis on green manufacturing, renewable energy projects, and advanced technology integration could help build a more resilient industrial base. These efforts aim to enhance productivity, reduce emissions, and position the UK as a leader in sustainable industrial development.

Conclusion

The UK’s Index of Production for September 2025 offers a cautiously positive picture of the nation’s industrial performance. With overall output rising 0.3% month-on-month and 1.4% year-on-year, the data points to slow but steady progress in key sectors.

Manufacturing remains the main growth driver, powered by transport and chemical production, while mining and quarrying provide additional support. Energy production, though weaker, reflects ongoing structural shifts rather than a fundamental decline.

In essence, the UK’s industrial sector appears to be regaining stability, underpinned by resilience, adaptability, and targeted policy support. While challenges remain, the latest figures highlight that Britain’s production base retains the strength and capacity needed to navigate an evolving global economic environment.