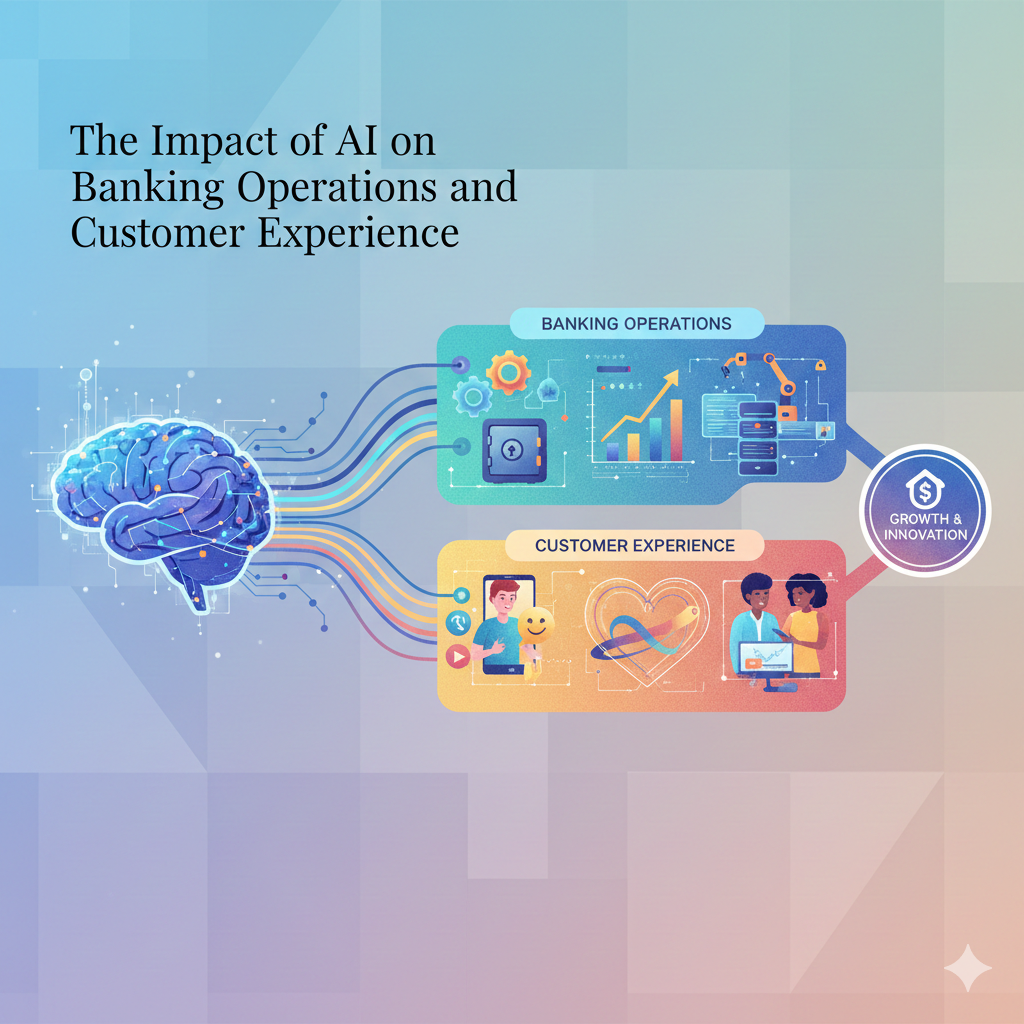

Artificial Intelligence (AI) has become a transformative force in the banking industry, reshaping how financial institutions operate, interact with customers, and manage risk. What was once considered an experimental technology is now a core part of banking strategies worldwide. As customer expectations rise and competition from fintech companies increases, banks are increasingly relying on AI to remain efficient, secure, and competitive. From improving customer service to strengthening fraud detection and enabling smarter decision-making, AI is redefining modern banking in meaningful ways.

One of the most significant reasons AI has become essential in banking is its ability to enhance customer experience. Today’s customers expect fast, personalized, and seamless banking services across digital platforms. AI-powered tools such as chatbots and virtual assistants allow banks to provide 24/7 customer support, answering common questions, resolving issues, and guiding users through transactions without long wait times. These systems can understand natural language, learn from previous interactions, and deliver increasingly accurate responses. As a result, customers receive quicker service, while banks reduce operational costs and free up human employees to focus on more complex tasks.

Beyond customer service, AI plays a crucial role in driving digital transformation within banks. Many traditional banks operate on legacy systems that are slow and inefficient. AI helps modernize these systems by automating processes, improving data analysis, and enabling real-time decision-making. Through AI-driven insights, banks can better understand customer behavior, predict needs, and offer tailored products such as personalized loans, savings plans, or investment advice. This level of personalization not only improves customer satisfaction but also strengthens long-term customer relationships and loyalty.

AI’s impact is especially powerful when combined with automation technologies. Robotic Process Automation (RPA) has long been used in banking to handle repetitive, rule-based tasks such as data entry or account reconciliation. When AI is added to automation, systems become more intelligent and capable of handling complex workflows. For example, an AI-enabled system can process a loan application by reviewing documents, assessing credit risk, detecting inconsistencies, and making recommendations—often with minimal human intervention. This speeds up approval times, reduces errors, and improves overall efficiency. Such intelligent automation allows banks to scale operations without significantly increasing costs.

Risk management is another area where AI has proven invaluable. Banks handle massive amounts of sensitive financial data and are constantly exposed to risks such as fraud, cyberattacks, and credit defaults. AI systems excel at analyzing large datasets to identify patterns that humans might miss. In fraud detection, AI models monitor transactions in real time, flagging suspicious activity based on unusual behavior or deviations from normal patterns. These systems can adapt quickly to new fraud tactics, making them far more effective than traditional rule-based approaches. As digital transactions continue to grow, AI-driven fraud prevention has become essential for protecting both banks and customers.

Credit scoring and lending decisions have also been significantly improved through AI. Traditional credit assessment methods often rely on limited data and rigid criteria, which can exclude certain individuals or small businesses. AI enables banks to analyze a wider range of data points, including transaction history and behavioral patterns, to assess creditworthiness more accurately. This leads to better lending decisions, reduced default rates, and increased financial inclusion. By using AI responsibly, banks can expand access to credit while maintaining strong risk controls.

In addition to operational and risk-related benefits, AI supports strategic decision-making in banking. Banks generate enormous volumes of data every day, but data alone has little value without meaningful insights. AI-powered analytics tools help banks transform raw data into actionable intelligence. These insights support better forecasting, portfolio management, and strategic planning. For example, AI can predict market trends, identify profitable customer segments, or recommend adjustments to investment strategies. This data-driven approach enables banks to respond more effectively to changing market conditions.

However, implementing AI in banking is not without challenges. One of the most important considerations is governance. Banks operate in a highly regulated environment, and the use of AI raises concerns related to transparency, fairness, data privacy, and accountability. Poorly designed AI systems can unintentionally introduce bias into decisions such as lending or hiring. To address these risks, banks must establish strong governance frameworks that ensure AI models are ethical, explainable, and compliant with regulations. Clear policies, regular audits, and human oversight are essential to building trust in AI systems.

Data governance is equally critical. AI systems rely on high-quality data to function effectively. Inconsistent, incomplete, or biased data can lead to inaccurate outcomes. Banks must invest in data management practices that ensure data accuracy, security, and privacy. This includes protecting customer information from cyber threats and ensuring compliance with data protection laws. As data becomes increasingly central to banking operations, strong data governance is a foundational requirement for successful AI adoption.

Another key aspect of AI implementation is workforce transformation. While AI automates many tasks, it does not eliminate the need for human expertise. Instead, it changes the nature of work. Employees must develop new skills to work alongside AI systems, interpret AI-generated insights, and make informed decisions. Banks that invest in reskilling and upskilling their workforce are better positioned to realize the full value of AI. By combining human judgment with machine intelligence, banks can achieve better outcomes than either could alone.

Looking to the future, AI opens the door to new opportunities for innovation and growth in banking. Emerging models such as embedded finance allow banking services to be integrated directly into non-financial platforms, such as retail or travel apps. AI enables these services by supporting real-time credit decisions, fraud checks, and personalized offers. Additionally, predictive analytics powered by AI helps banks anticipate customer needs and proactively offer solutions, creating a more seamless and intuitive banking experience.

AI also supports sustainable growth by improving efficiency and reducing waste. Automated processes consume fewer resources, while improved risk management minimizes financial losses. Over time, these efficiencies contribute to stronger financial performance and greater resilience. As technology continues to evolve, banks that embrace AI responsibly will be better equipped to adapt to future challenges and opportunities.

In conclusion, Artificial Intelligence has become a fundamental pillar of modern banking. It enhances customer experience, drives digital transformation, improves risk management, and supports smarter decision-making. While challenges related to governance, ethics, and workforce readiness remain, these can be addressed through thoughtful strategy and responsible implementation. Banks that successfully integrate AI into their operations are not only improving efficiency but also redefining what banking looks like in the digital age. As AI continues to advance, its role in shaping the future of banking will only grow stronger.