Rohan had just received his salary message.

“₹42,500 credited,” the SMS flashed.

Like every month, the money felt enough for only rent, food, EMIs, and weekend outings. Savings? Almost zero.

That evening, while having chai at the office tapri, his senior colleague, Mehul, said something that stuck in his mind forever:

“Rohan, you don’t become rich by saving big.

You become rich by saving small — but saving early.”

Rohan smiled and replied,

“Arre Mehul bhai, I can barely save ₹150 a day. What difference will that make?”

Mehul looked at him, sipped his tea, and said:

“₹150 a day can make you a crorepati.

That’s the magic of compounding.”

Rohan didn’t believe him.

A crore from ₹150/day? Impossible… right?

⭐ The Day Rohan Discovered Compounding

The next day, Mehul called Rohan to his desk and showed him a simple chart.

He said, “Look, Rohan. You don’t need big money. You need time + consistency.”

He opened a calculator and showed this table:

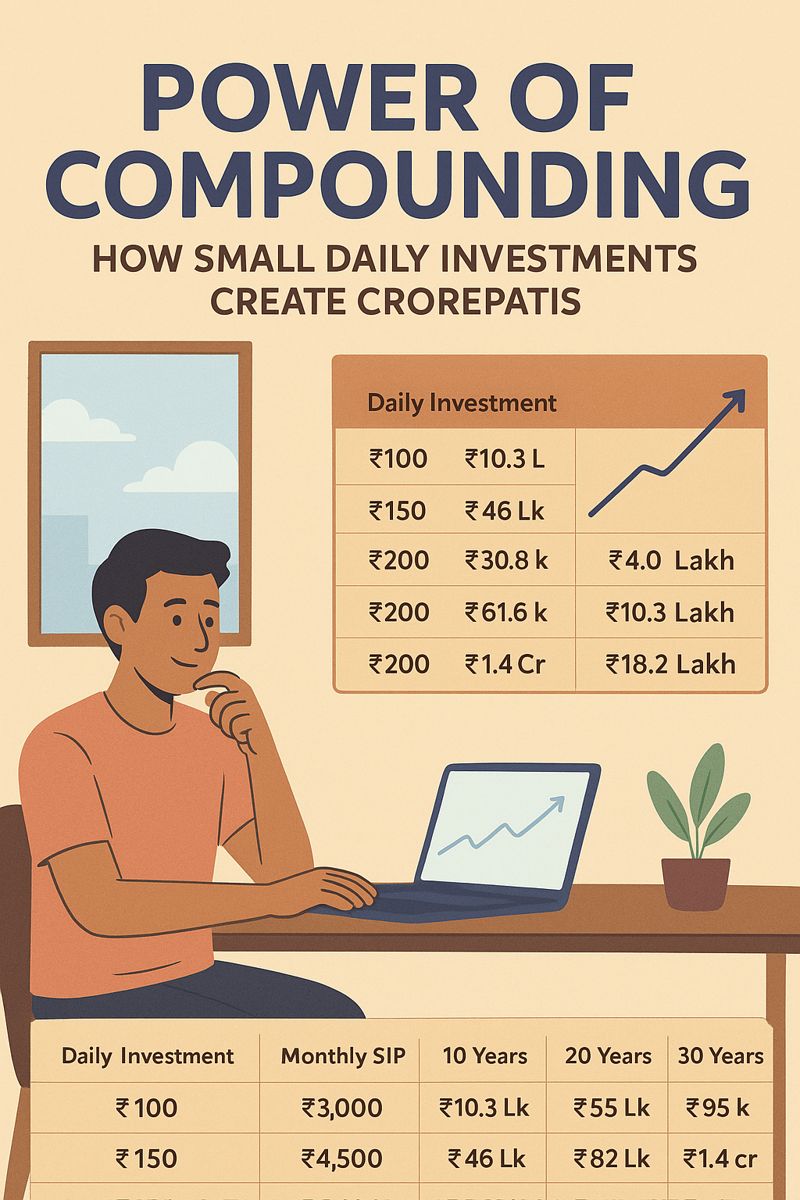

📊 Table: How Small Daily SIPs Grow Over Time (At 12% Annual Returns)

| Daily Investment | Monthly SIP | 10 Years | 20 Years | 25 Years | 30 Years |

|---|---|---|---|---|---|

| ₹100/day | ₹3,000 | ₹6.9 L | ₹30.8 L | ₹55 L | ₹95 L |

| ₹150/day | ₹4,500 | ₹10.3 L | ₹46 L | ₹82 L | ₹1.4 Cr |

| ₹200/day | ₹6,000 | ₹13.8 L | ₹61.6 L | ₹1.1 Cr | ₹1.8 Cr |

Rohan’s eyes widened.

He whispered, “₹150/day becomes ₹1.4 crore?”

Mehul nodded.

“Yes, only if you allow compounding to do its job. Don’t stop your SIPs. Don’t panic during market falls. Just stay invested.”

Rohan felt something change inside him.

For the first time, he saw hope — that even an ordinary salaried person like him could build extraordinary wealth.

⭐ Rohan Starts His Journey

That night, Rohan sat on his bed and thought:

- “I spend ₹150/day on snacks.”

- “I spend ₹2,000/month on impulsive food delivery.”

- “But I can’t save ₹4,500 for my future?”

The next morning, without overthinking, he started a ₹150/day SIP (₹4,500/month) in an equity mutual fund.

He promised himself:

“No matter what, I won’t stop this SIP.”

Year after year, he continued investing.

Some years markets went up — he felt excited.

Some years markets went down — he felt scared.

But he stayed disciplined.

He remembered Mehul’s line:

“Compounding is slow in the beginning… and then suddenly very fast.”

⭐ 10 Years Later: The First Shock

Rohan checked his investment app.

He had invested:

₹4,500 × 120 months = ₹5.4 lakh

His fund value was around:

₹10.3 lakh

“Double? Seriously?” he thought.

That day, he didn’t buy an expensive phone.

He increased his SIP by another ₹1,000.

⭐ 20 Years Later: The Big Turning Point

Rohan was now married, had a daughter, and earned a good salary.

Life looked different — stable, peaceful.

His SIP of ₹4,500/day (plus small increases every year) was now worth around:

₹45–50 lakh

Even though his job didn’t make him rich fast,

his consistency did.

⭐ 25 Years Later: Rohan Became a Crorepati

One ordinary evening, Rohan opened his investment summary.

The number on the screen made him breathe heavily.

₹1,40,00,000+

(one crore forty lakh)

He had become a crorepati.

Not through luck.

Not through high income.

Not through risky trades.

But through Compounding + Discipline + Time.

He messaged Mehul:

“Bhai… your ₹150 advice made me a crorepati today.”

Mehul replied with a smiling emoji:

“I told you. Small steps create big futures.”

⭐ Simple Diagram That Changed Rohan’s Life

Year 1–10: Growth is slow (Looks boring)

Year 11–20: Growth becomes noticeable

Year 21–30: Growth explodes (Crorepati zone)

⭐ Moral of Rohan’s Story

You don’t need:

❌ big income

❌ big savings

❌ big risks

You need:

✔ small daily investment

✔ patience

✔ discipline

✔ time

₹150 a day is not money —

it’s a seed that becomes a tree.

⭐ Your Takeaway

If you start today with:

₹100/day → You can reach ₹95 lakh

₹150/day → You can cross ₹1.4 crore

₹200/day → You can touch nearly ₹2 crore

Your future self will thank you.

Imagine your child asking,

“Papa/Mumma, how did you save so much?”

And you smiling and saying,

“I just invested ₹150/day.”