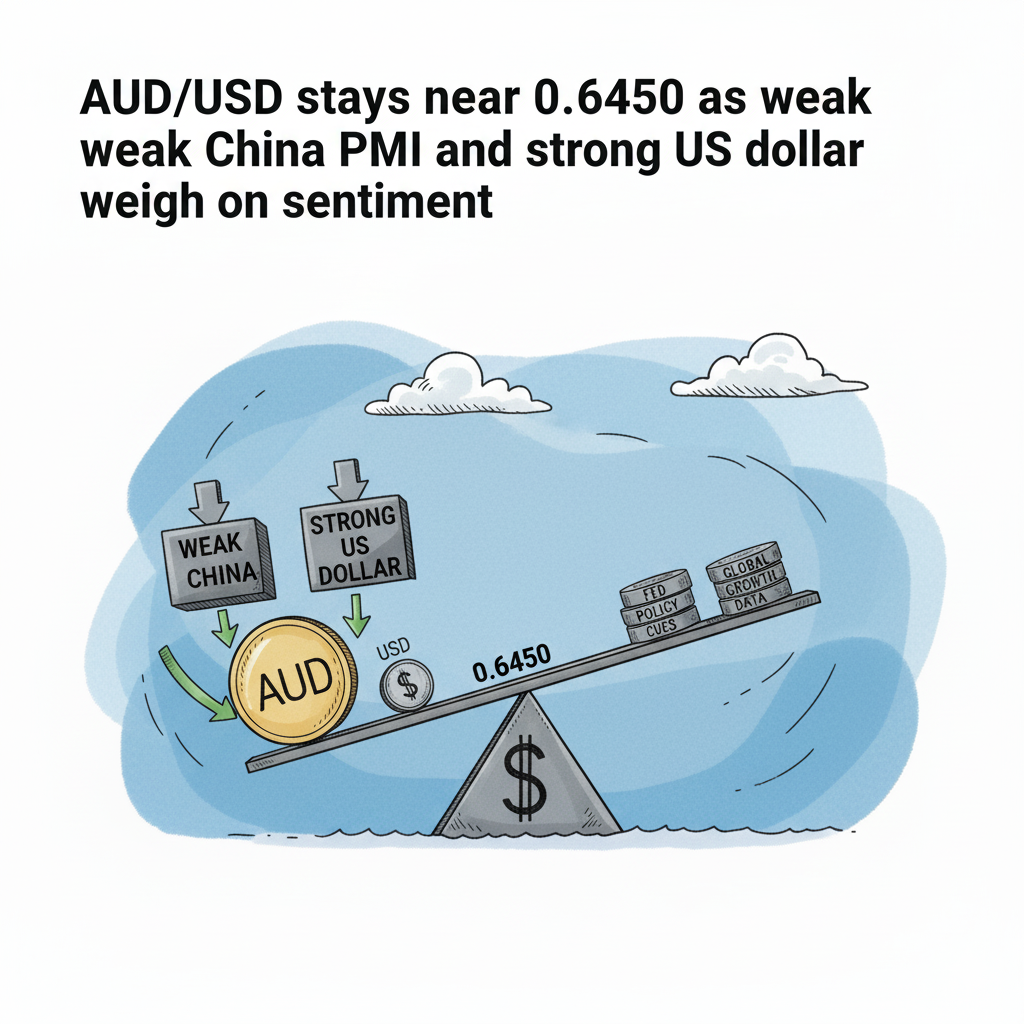

The Australian dollar (AUD) has remained under mild pressure this week, with the AUD/USD pair hovering near the 0.6450 mark, reflecting investor caution and muted risk appetite. As global traders digest weak Chinese economic data and a resilient US dollar, the Aussie is struggling to find solid footing. The interplay of global macro factors, monetary policy expectations, and technical resistance is keeping the pair range-bound.

Let’s unpack the key drivers behind the current market tone and what investors should watch moving forward.

Muted Sentiment Following China’s PMI Data

At the heart of the recent weakness in the Australian dollar lies China’s latest RatingDog Services PMI, which dropped slightly to 52.6 in October from 52.9 in September. While the reading still indicates expansion (as it remains above 50), the slowdown in China’s services sector underscores the challenges facing the world’s second-largest economy.

For Australia, this data matters deeply. China is its largest trading partner, accounting for a significant portion of exports — from iron ore and coal to agricultural products. Any signal of deceleration in Chinese demand tends to ripple across Australian markets, putting downward pressure on the currency. The softer PMI data served as a reminder that China’s recovery remains uneven, and that’s directly translating into tepid sentiment toward the Aussie dollar.

Australia’s Domestic Data Fails to Inspire

On the domestic front, Australia’s own services and composite PMI figures stayed above the key 50-point mark, signaling ongoing expansion. However, growth was modest, suggesting that while the economy continues to hold up, it lacks strong momentum. The Reserve Bank of Australia (RBA) has adopted a cautious tone, recognizing that inflation remains sticky but the labor market is showing signs of cooling.

This cautious approach by the RBA contrasts sharply with the firmness of the US Federal Reserve, creating a monetary policy divergence that weighs on the AUD. Traders perceive that while the RBA is unlikely to hike rates further, the Fed remains in a holding pattern, keeping rates elevated for longer to ensure inflation is fully under control.

That expectation supports the US dollar — and indirectly limits the Aussie’s recovery.

China’s Trade Gesture Provides Limited Relief

There was some positive news from Beijing this week: China announced plans to suspend certain tariffs on US agricultural goods starting November 10. This move was viewed as a modest step toward improving global trade relations and possibly stabilizing broader market sentiment.

For Australia, however, the relief was short-lived. While improved trade dynamics between the US and China can support global growth, they don’t immediately boost Australian exports. Traders instead see this as a signal of cautious optimism, but not enough to alter the short-term bearish bias on AUD/USD.

The US Dollar: The Dominant Counterforce

Perhaps the biggest reason for the AUD/USD pair’s subdued tone is the resilience of the US dollar. The greenback remains supported by a combination of robust US economic data, persistent inflationary pressure, and reduced expectations for near-term Federal Reserve rate cuts.

The latest US macro indicators — particularly labor market figures and manufacturing surveys — have shown resilience, keeping Treasury yields elevated and the dollar in demand. The Federal Reserve’s patient stance reinforces the view that US monetary conditions will remain tight well into 2026, even as other central banks begin to consider easing.

This environment makes it difficult for risk-sensitive currencies like the Aussie to make meaningful gains. Until there’s a visible shift in US data or Fed communication, the dollar’s dominance will likely cap AUD/USD’s upside.

Technical Picture: Range-Bound with Modest Support

Technically, the AUD/USD pair is consolidating within a well-defined range between 0.6400 and 0.6700. Immediate resistance is visible near 0.6500, while strong support lies around 0.6460 and 0.6414.

The 50-day and 100-day moving averages are converging, indicating a lack of strong directional bias. Momentum oscillators such as the RSI (Relative Strength Index) are neutral, signaling that the pair is neither overbought nor oversold.

For traders, this setup translates into a “wait-and-see” environment. Breakouts beyond 0.6500 could attract short-term buying, potentially targeting 0.6600, while a drop below 0.6400 may trigger further weakness toward 0.6350. Until a strong catalyst emerges, the Aussie appears locked in consolidation mode.

Market Psychology: Risk Aversion in Play

Beyond technicals and data, market sentiment remains fragile. Investors continue to exhibit a risk-off tone amid concerns over global growth, geopolitical tensions, and uncertainty surrounding the path of monetary policy in major economies.

The Australian dollar is traditionally viewed as a risk-sensitive currency, meaning it tends to fall when investors shy away from riskier assets like equities and emerging market currencies. The recent downturn in global equities and soft commodity demand has further reinforced the cautious tone in AUD/USD trading.

That said, long-term investors see value in the Aussie around current levels. Historically, when the currency trades near the lower end of its medium-term range, it tends to attract strategic buying interest from global funds seeking diversification and exposure to resource-driven growth.

Outlook: Waiting for a Catalyst

Looking ahead, the path for AUD/USD will largely depend on two key factors:

- US economic data releases — particularly the upcoming private payroll and inflation figures.

- China’s growth momentum — whether Beijing can stabilize its manufacturing and property sectors.

If Chinese data show signs of improvement and the Fed hints at a softer stance, we could see a gradual recovery toward 0.6600–0.6700. However, if US yields remain high and Chinese growth disappoints, the pair may revisit the 0.6400–0.6350 zone in the coming weeks.

Traders should also keep an eye on commodity prices — especially iron ore and copper — as both serve as leading indicators for the Australian economy. A sustained rebound in commodities could lend the Aussie much-needed support.

Investor Takeaway

For investors, the current price zone presents both challenge and opportunity. On one hand, subdued price action reflects global uncertainty and the dominance of the US dollar. On the other, the Australian dollar’s resilience above 0.6400 suggests a base is forming — possibly setting the stage for a recovery if conditions improve.

In the medium term, AUD/USD remains a story of global balance — between US monetary strength and China’s economic health. Traders with a long-term horizon may find value in gradually accumulating AUD positions near current levels, while short-term participants may continue to trade within the established range.

Final Thoughts

The Australian dollar’s current behavior encapsulates the broader global market mood — cautious, watchful, and highly reactive to data. As a stock and forex analyst, I see AUD/USD’s subdued movement near 0.6450 as reflective of competing narratives: optimism for eventual recovery offset by the reality of strong US fundamentals and China’s uneven growth.

Until clarity emerges from both Washington and Beijing, the Aussie dollar is likely to remain in a holding pattern — a currency waiting for its next catalyst. For now, traders should respect the range, watch key data releases, and stay nimble.