Title: Inflation: Why Money Supply, Not Corporate Profits, Holds the Real Power

In recent years, the debate around inflation has become louder than ever. Many people point fingers at large corporations, accusing them of excessive greed and inflated profit margins as the main culprit behind soaring prices. This narrative, often dubbed “greedflation,” has captured headlines, political speeches, and even social media debates. But as any seasoned market observer or investor knows, the truth behind inflation runs much deeper — and much more complex — than just corporate behavior.

As a market analyst who’s spent years watching the ebb and flow of prices, currencies, and consumer sentiment, I can say with confidence: the expansion of the money supply, not corporate profits, is the real engine driving inflation.

The Misplaced Blame: Are Companies Really Causing Inflation?

Let’s start by dissecting the popular narrative. Many assume that corporations, driven by greed, simply raise prices to earn more money. It sounds simple and emotionally satisfying — especially when consumers feel the pain of higher grocery bills, rent, or fuel prices. But economics isn’t governed by emotions; it’s ruled by fundamentals.

In a functioning market, companies can’t just increase prices at will. Prices are not set in isolation — they’re the result of a delicate negotiation between sellers who want to maximize profit and buyers who aim to minimize spending. If a company decides to double the price of its product overnight, but customers aren’t willing to pay that premium, sales will drop, and profits will shrink. That’s not greed; that’s market discipline.

So, blaming corporate profit margins for persistent inflation is like blaming a thermometer for a fever. Profits might rise during inflationary periods, but they’re not what’s causing prices to rise across the board.

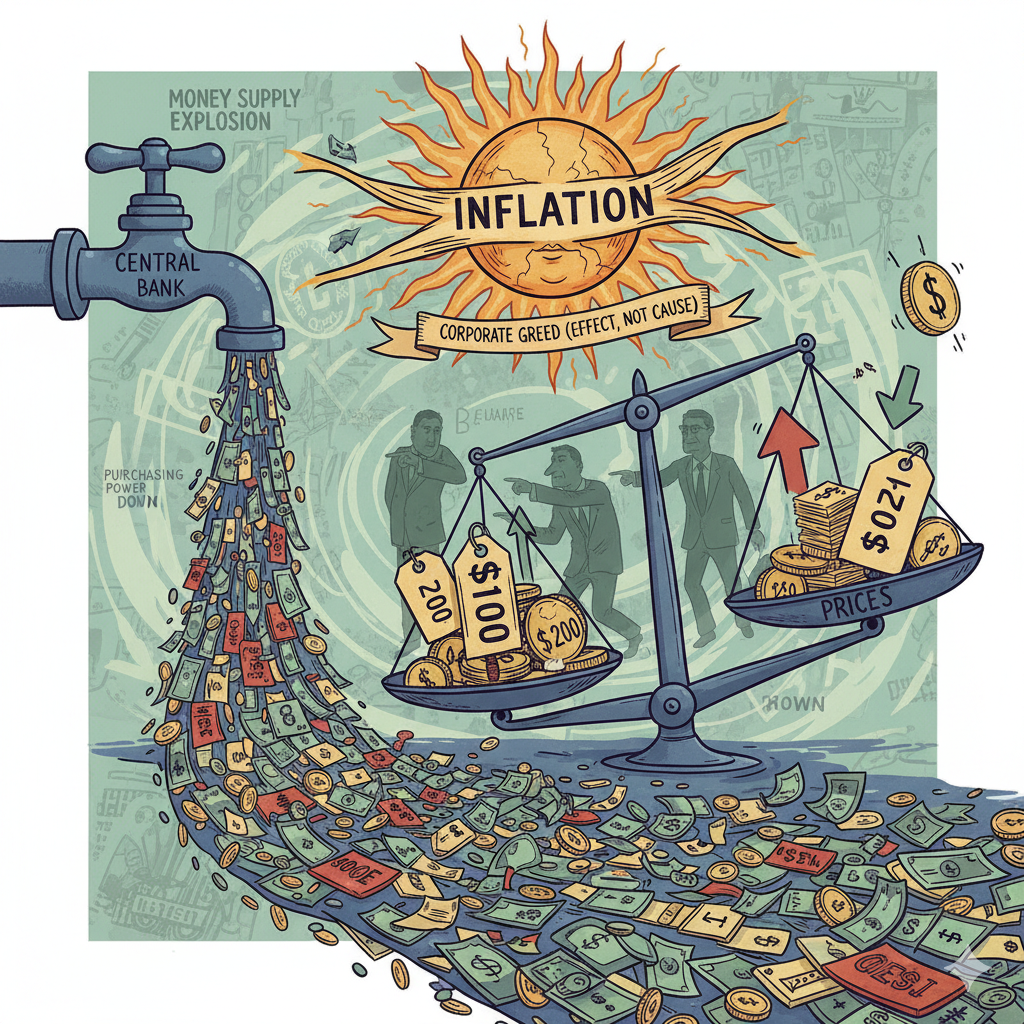

The Real Driver: Expansion of the Money Supply

To understand inflation, we must turn our attention to monetary policy — the invisible force that shapes the value of every dollar, rupee, or euro we hold. When central banks increase the money supply, they effectively create more purchasing power in the economy. But if the amount of goods and services doesn’t grow at the same pace, the balance between money and goods shifts — leading to higher prices.

Think of it this way: if there are 100 goods in an economy and $100 circulating, each good roughly costs $1. But if the money supply doubles to $200 while the number of goods remains 100, prices will naturally adjust upward to reflect the new equilibrium. Each good might now cost $2. That’s inflation in its purest form — a monetary imbalance, not corporate conspiracy.

In this sense, inflation is less about producers deciding to raise prices and more about the currency itself losing value. The more money that’s printed or injected into circulation without productivity growth, the weaker its purchasing power becomes.

Early Recipients Benefit First

One of the less discussed but crucial effects of money supply expansion is the “Cantillon Effect.” This concept explains that when new money enters the economy, it doesn’t reach everyone equally or simultaneously.

Those who receive the new money first — often government contractors, banks, or large institutions — get to spend it while prices are still relatively low. As this new money circulates and filters down to the broader public, demand increases and prices rise. By the time the average consumer or small business feels the effect, prices have already climbed, and their real purchasing power has declined.

In other words, inflation quietly redistributes wealth — benefiting those closest to the source of new money while hurting those at the end of the economic chain.

Why Corporate Profits Rise During Inflationary Periods

If corporate profits rise during inflation, it’s often a symptom rather than a cause. When money supply expands, consumer demand increases, at least temporarily. Companies may sell more goods at higher nominal prices, boosting revenue figures. However, these higher profits are often illusory — when adjusted for inflation, the real gains are far smaller.

For example, a company’s revenue may rise 10% year-on-year, but if inflation is running at 8%, the real growth is barely 2%. Meanwhile, input costs — wages, raw materials, logistics — also rise, squeezing margins. So, while it may appear that companies are profiting from inflation, in reality, they are often struggling to maintain profitability amid volatile costs and uncertain demand.

The Danger of Policy Missteps

When policymakers misdiagnose inflation, the solutions they propose often make the problem worse. Blaming corporate greed leads to price controls — restrictions that force companies to sell goods below market value. While such measures may sound appealing to consumers, they tend to backfire.

Price controls create shortages because producers lose the incentive to produce at unprofitable rates. Shelves empty, black markets thrive, and quality deteriorates. History has shown this repeatedly, from Venezuela’s grocery shortages to the U.S. fuel lines of the 1970s.

The only sustainable way to combat inflation is to control the growth of money supply and ensure that monetary expansion aligns with real economic productivity.

Investors’ Perspective: Navigating an Inflationary Landscape

As an investor, understanding the true cause of inflation helps you make smarter portfolio decisions. During inflationary periods driven by money supply growth, hard assets like gold, silver, real estate, and commodities tend to perform well. These assets preserve value as currencies weaken.

Meanwhile, long-term bonds and fixed-income instruments usually underperform because their returns are eroded by rising prices. Equity markets can offer protection, but only selectively — businesses with strong pricing power, low debt, and essential products tend to fare better than highly leveraged or speculative companies.

In essence, inflation reshuffles the investment landscape. The winners are those who understand where real value lies — not in nominal profits, but in purchasing power preservation.

The Bottom Line: It’s the Money, Not the Markets

The next time you see a headline blaming corporations for inflation, remember that markets don’t operate in a vacuum. Prices reflect the interaction of countless decisions by buyers and sellers, all influenced by one overarching factor — the quantity and value of money circulating in the system.

Corporate profits may fluctuate with inflation, but they are not the root cause. The real culprit is an overactive money supply, driven by policies that inject liquidity faster than the economy can absorb it.

Until policymakers recognize that controlling inflation means controlling money creation, we’ll continue to see cycles of price surges, political blame games, and misguided economic solutions.

As a market participant, the best strategy is not to look for villains but to understand the mechanics — because those who grasp the real forces behind inflation can protect their wealth, navigate volatility, and even find opportunity in chaos.

In short: Inflation isn’t a story of corporate greed — it’s a lesson in monetary discipline. And in finance, as in life, understanding what’s really driving the numbers makes all the difference.

In recent years, the debate around inflation has become louder than ever. Many people point fingers at large corporations, accusing them of excessive greed and inflated profit margins as the main culprit behind soaring prices. This narrative, often dubbed “greedflation,” has captured headlines, political speeches, and even social media debates. But as any seasoned market observer or investor knows, the truth behind inflation runs much deeper — and much more complex — than just corporate behavior.

As a market analyst who’s spent years watching the ebb and flow of prices, currencies, and consumer sentiment, I can say with confidence: the expansion of the money supply, not corporate profits, is the real engine driving inflation.

The Misplaced Blame: Are Companies Really Causing Inflation?

Let’s start by dissecting the popular narrative. Many assume that corporations, driven by greed, simply raise prices to earn more money. It sounds simple and emotionally satisfying — especially when consumers feel the pain of higher grocery bills, rent, or fuel prices. But economics isn’t governed by emotions; it’s ruled by fundamentals.

In a functioning market, companies can’t just increase prices at will. Prices are not set in isolation — they’re the result of a delicate negotiation between sellers who want to maximize profit and buyers who aim to minimize spending. If a company decides to double the price of its product overnight, but customers aren’t willing to pay that premium, sales will drop, and profits will shrink. That’s not greed; that’s market discipline.

So, blaming corporate profit margins for persistent inflation is like blaming a thermometer for a fever. Profits might rise during inflationary periods, but they’re not what’s causing prices to rise across the board.

The Real Driver: Expansion of the Money Supply

To understand inflation, we must turn our attention to monetary policy — the invisible force that shapes the value of every dollar, rupee, or euro we hold. When central banks increase the money supply, they effectively create more purchasing power in the economy. But if the amount of goods and services doesn’t grow at the same pace, the balance between money and goods shifts — leading to higher prices.

Think of it this way: if there are 100 goods in an economy and $100 circulating, each good roughly costs $1. But if the money supply doubles to $200 while the number of goods remains 100, prices will naturally adjust upward to reflect the new equilibrium. Each good might now cost $2. That’s inflation in its purest form — a monetary imbalance, not corporate conspiracy.

In this sense, inflation is less about producers deciding to raise prices and more about the currency itself losing value. The more money that’s printed or injected into circulation without productivity growth, the weaker its purchasing power becomes.

Early Recipients Benefit First

One of the less discussed but crucial effects of money supply expansion is the “Cantillon Effect.” This concept explains that when new money enters the economy, it doesn’t reach everyone equally or simultaneously.

Those who receive the new money first — often government contractors, banks, or large institutions — get to spend it while prices are still relatively low. As this new money circulates and filters down to the broader public, demand increases and prices rise. By the time the average consumer or small business feels the effect, prices have already climbed, and their real purchasing power has declined.

In other words, inflation quietly redistributes wealth — benefiting those closest to the source of new money while hurting those at the end of the economic chain.

Why Corporate Profits Rise During Inflationary Periods

If corporate profits rise during inflation, it’s often a symptom rather than a cause. When money supply expands, consumer demand increases, at least temporarily. Companies may sell more goods at higher nominal prices, boosting revenue figures. However, these higher profits are often illusory — when adjusted for inflation, the real gains are far smaller.

For example, a company’s revenue may rise 10% year-on-year, but if inflation is running at 8%, the real growth is barely 2%. Meanwhile, input costs — wages, raw materials, logistics — also rise, squeezing margins. So, while it may appear that companies are profiting from inflation, in reality, they are often struggling to maintain profitability amid volatile costs and uncertain demand.

The Danger of Policy Missteps

When policymakers misdiagnose inflation, the solutions they propose often make the problem worse. Blaming corporate greed leads to price controls — restrictions that force companies to sell goods below market value. While such measures may sound appealing to consumers, they tend to backfire.

Price controls create shortages because producers lose the incentive to produce at unprofitable rates. Shelves empty, black markets thrive, and quality deteriorates. History has shown this repeatedly, from Venezuela’s grocery shortages to the U.S. fuel lines of the 1970s.

The only sustainable way to combat inflation is to control the growth of money supply and ensure that monetary expansion aligns with real economic productivity.

Investors’ Perspective: Navigating an Inflationary Landscape

As an investor, understanding the true cause of inflation helps you make smarter portfolio decisions. During inflationary periods driven by money supply growth, hard assets like gold, silver, real estate, and commodities tend to perform well. These assets preserve value as currencies weaken.

Meanwhile, long-term bonds and fixed-income instruments usually underperform because their returns are eroded by rising prices. Equity markets can offer protection, but only selectively — businesses with strong pricing power, low debt, and essential products tend to fare better than highly leveraged or speculative companies.

In essence, inflation reshuffles the investment landscape. The winners are those who understand where real value lies — not in nominal profits, but in purchasing power preservation.

The Bottom Line: It’s the Money, Not the Markets

The next time you see a headline blaming corporations for inflation, remember that markets don’t operate in a vacuum. Prices reflect the interaction of countless decisions by buyers and sellers, all influenced by one overarching factor — the quantity and value of money circulating in the system.

Corporate profits may fluctuate with inflation, but they are not the root cause. The real culprit is an overactive money supply, driven by policies that inject liquidity faster than the economy can absorb it.

Until policymakers recognize that controlling inflation means controlling money creation, we’ll continue to see cycles of price surges, political blame games, and misguided economic solutions.

As a market participant, the best strategy is not to look for villains but to understand the mechanics — because those who grasp the real forces behind inflation can protect their wealth, navigate volatility, and even find opportunity in chaos.

In short: Inflation isn’t a story of corporate greed — it’s a lesson in monetary discipline. And in finance, as in life, understanding what’s really driving the numbers makes all the difference.

One thought on “Inflation: Why Money Supply, Not Corporate Profits, Holds the Real Power”

Comments are closed.