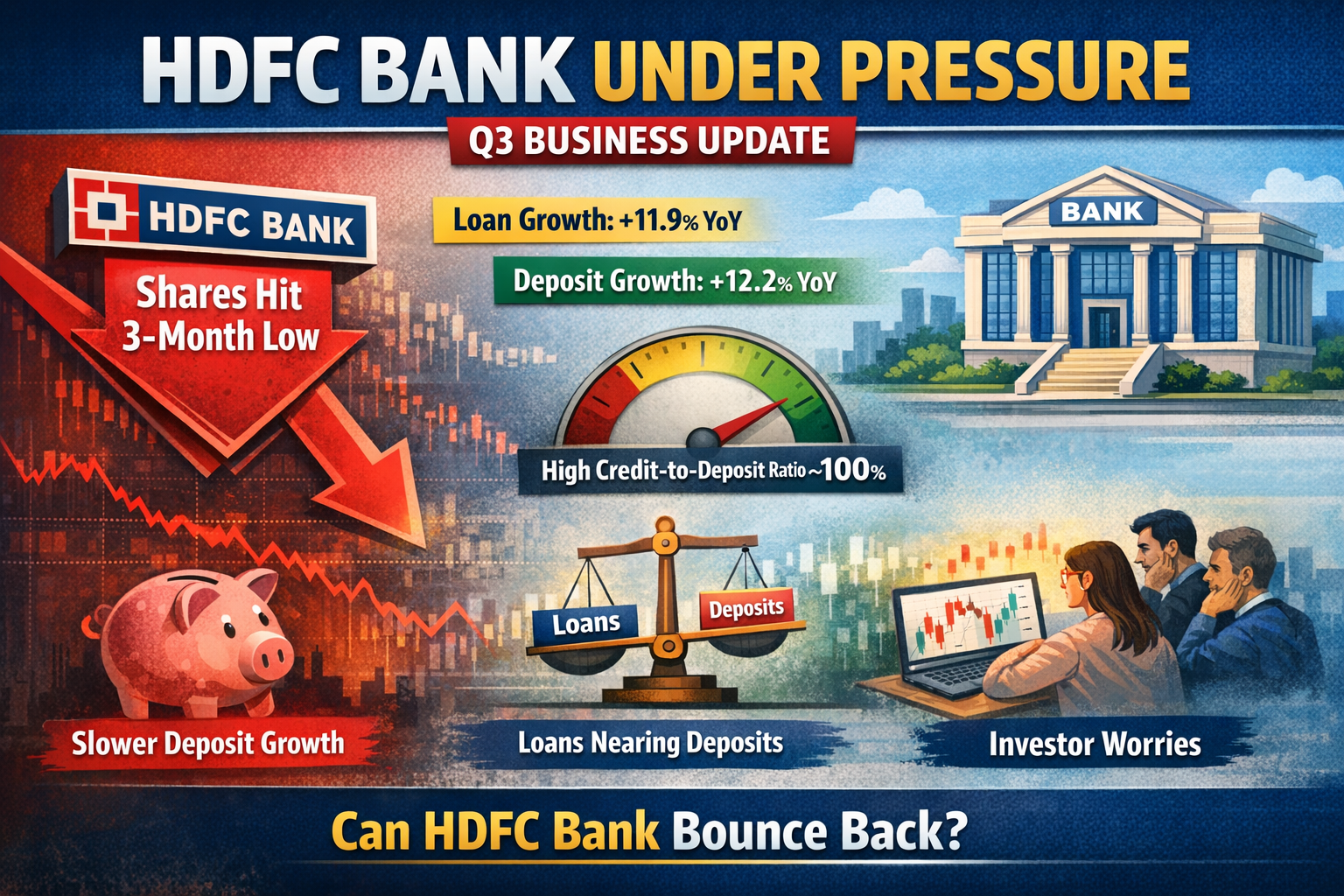

HDFC Bank, India’s largest private sector lender, saw its share price fall sharply after releasing its Q3 business update, with the stock hitting a three-month low. Despite reporting steady growth in loans and deposits, the market reaction was negative, leaving many investors wondering: what went wrong?

A closer look at the numbers and brokerage commentary reveals that while the bank’s core business remains strong, slower deposit growth and balance sheet pressures raised concerns among analysts.

Stock Market Reaction: Why the Fall?

Following the Q3 business update, HDFC Bank shares dropped over 2%, underperforming the broader banking index. The decline pushed the stock to its lowest level in three months, signaling investor disappointment.

The fall was not triggered by poor growth numbers but rather by expectations versus reality. Markets were hoping for a stronger pickup in deposits after the merger-related slowdown, which did not fully materialize.

Advances Growth: Still Healthy but Moderating

On the lending front, HDFC Bank delivered steady growth, though not enough to impress the Street.

- Average advances grew 9% year-on-year, reaching around ₹28.64 lakh crore in Q3.

- Period-end advances under management increased by 9.8% YoY.

- Gross advances rose 11.9% YoY, showing healthy demand for credit across segments.

These figures indicate that loan demand remains intact, supported by retail, SME, and corporate borrowing. However, analysts noted that loan growth is now increasingly constrained by funding availability rather than demand.

Deposits: The Core Area of Concern

The biggest worry for investors was deposit growth, which lagged expectations.

- Average deposits increased 12.2% YoY to ₹27.52 lakh crore.

- CASA (Current Account Savings Account) deposits grew 9.9% YoY to ₹8.18 lakh crore.

While these numbers look decent on paper, brokerages pointed out that deposit growth is not fast enough to support aggressive loan expansion. CASA growth, in particular, remains under pressure due to intense competition among banks and rising fixed deposit rates.

Credit-to-Deposit Ratio Near 100%

One of the most closely watched metrics, the credit-to-deposit (CD) ratio, has climbed close to 100%. This means HDFC Bank is lending out nearly all the money it is mobilizing through deposits.

A high CD ratio is not immediately alarming but does limit flexibility. It suggests:

- The bank has less room to grow loans without accelerating deposit collection.

- Funding costs may stay elevated, impacting margins.

Brokerages flagged this as a key overhang on near-term performance.

What Brokerages Are Saying

Brokerage views on HDFC Bank remain mixed, with long-term confidence intact but short-term caution.

- Motilal Oswal maintained a ‘Buy’ rating, citing stable advances growth and the bank’s strong franchise. It believes deposit traction should gradually improve as merger synergies kick in.

- Nomura, however, highlighted concerns around slower deposit mobilisation, warning that it could cap loan growth and pressure profitability in the near term.

Most analysts agree that while fundamentals are solid, expectations need to reset for the next few quarters.

Why the Market Is Being Extra Critical

HDFC Bank has historically been valued at a premium due to its consistent growth, strong asset quality, and superior execution. As a result, even small disappointments trigger sharp reactions.

Investors were hoping the bank would bounce back faster after the HDFC Ltd merger, especially on deposits. The Q3 update showed progress, but not at the pace the market had priced in.

Long-Term Outlook: Still Strong?

Despite the near-term concerns, the long-term story for HDFC Bank remains intact:

- Strong retail and corporate franchise

- Best-in-class risk management

- Large distribution network

- Gradual normalization post-merger

Analysts expect deposit growth to improve gradually as system liquidity eases and the bank recalibrates its pricing strategy.

What Should Investors Do?

For long-term investors, the recent correction could be an opportunity to accumulate a fundamentally strong banking stock at relatively reasonable valuations.

For short-term traders, however, the stock may remain under pressure until:

- Deposit growth improves

- CD ratio moderates

- Clear margin visibility emerges

Final Takeaway

HDFC Bank’s Q3 business update was not weak, but it fell short of high market expectations. Slower deposit growth and a tight funding position overshadowed otherwise stable advances growth, leading to a sharp sell-off.

While near-term challenges persist, the bank’s long-term fundamentals remain solid. As deposit momentum picks up over the coming quarters, investor confidence is likely to return.*