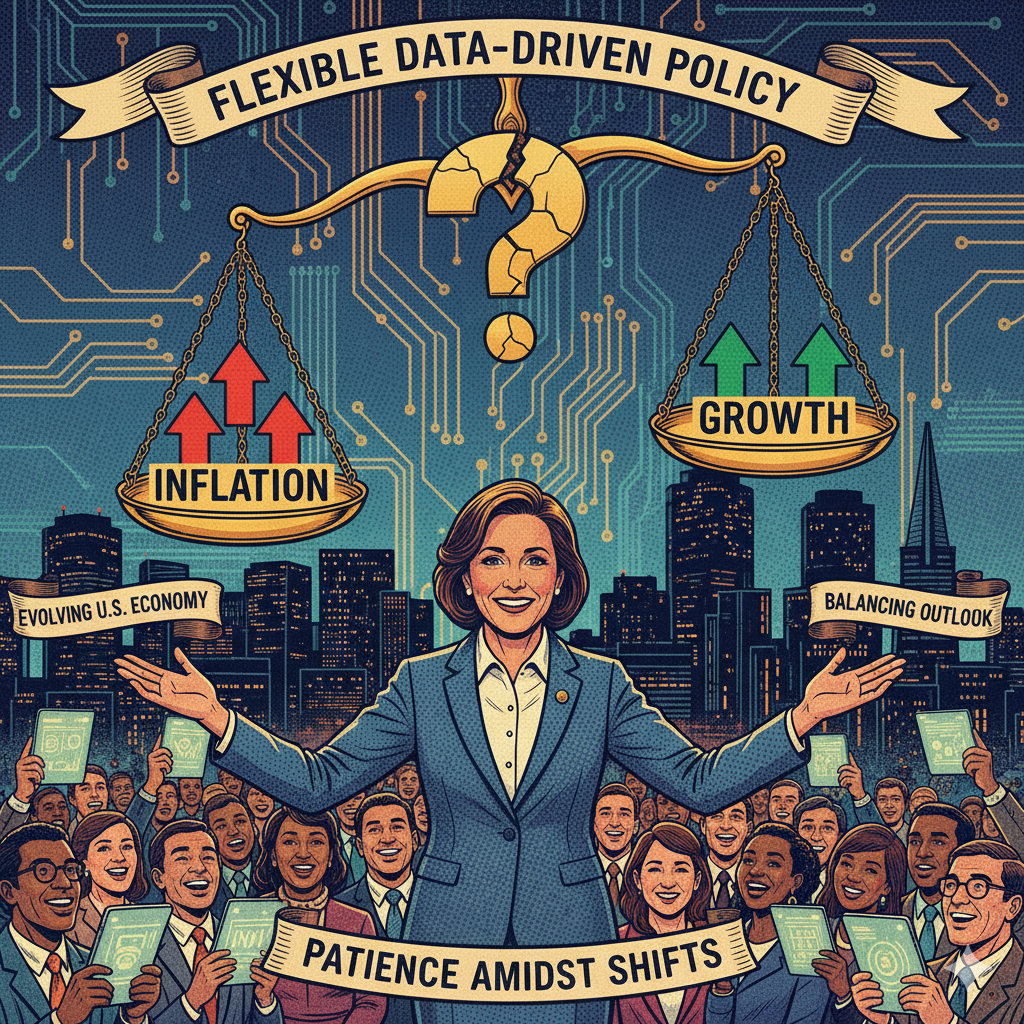

In the ever-shifting world of economics, the role of central bankers has never been more complex. Mary Daly, President of the Federal Reserve Bank of San Francisco, recently addressed this reality with striking clarity. Her remarks, delivered in a thoughtful and measured tone, outlined how U.S. monetary policy must evolve in a world marked by inflationary persistence, shifting labor market dynamics, and growing uncertainty. Daly’s speech, titled “Policymaking Amid Change,” offers deep insight into how the Federal Reserve views the path ahead — one defined by balance, flexibility, and an unwavering commitment to stability.

A Balancing Act in an Uncertain Economy

Daly began by acknowledging the resilience of the U.S. economy. Despite multiple headwinds — global instability, supply chain challenges, and high borrowing costs — growth has held up better than expected. The labor market, too, remains robust, even as it shows subtle signs of cooling. However, she was quick to point out that this balance is fragile. Inflation, though lower than its 2022 peak, continues to hover above the Fed’s 2% target, keeping policymakers on alert.

According to Daly, this situation places the Federal Reserve in a “delicate position.” On one hand, overly restrictive policies could slow down economic momentum and risk a downturn. On the other, premature easing could reignite inflationary pressures, undermining the progress made so far. The challenge, as Daly sees it, lies in maintaining this equilibrium — a task that requires both patience and precision.

She explained that while data continues to show broad resilience, the signs of moderation in the job market and consumer spending indicate that policy tightening is having its intended effect. Yet, these outcomes are uneven across sectors and demographics, underscoring the need for a nuanced approach rather than a one-size-fits-all policy.

Inflation: The Persistent Challenge

At the heart of Daly’s message was the Federal Reserve’s ongoing battle against inflation. While consumer price growth has slowed from the extremes of 2022, progress has been uneven. Daly emphasized that inflation remains “stubbornly above target,” particularly in services, where wage and price pressures continue to linger.

She noted that while energy prices have stabilized, underlying core inflation — which excludes volatile components like food and energy — continues to show resistance. This stickiness suggests that the road to price stability will be gradual, not linear. “Inflation does not move in a straight line,” Daly remarked, adding that temporary setbacks should not distract policymakers from their long-term objectives.

Her message was clear: the Federal Reserve must remain vigilant. Even as markets speculate about future rate cuts, Daly argued that it is too early to declare victory. The central bank, she said, will continue to rely on a wide range of indicators to ensure that inflation expectations remain anchored and that real progress toward the 2% target is sustainable.

Navigating Data Gaps and Uncertainty

One of the more practical challenges Daly addressed was the potential for government shutdowns or data disruptions — events that could limit access to key economic indicators. In such situations, she explained, the Federal Reserve can turn to alternative data sources. Private sector surveys, financial market readings, and real-time analytics can offer timely insights even when official reports are delayed.

This adaptability reflects a broader theme in Daly’s speech — that policymaking in today’s environment requires flexibility. The economy, she said, is no longer governed by predictable cycles. Structural changes, including technological innovation, demographic shifts, and evolving global trade patterns, have altered the traditional playbook. As such, policymakers must remain alert and ready to adjust course as new information emerges.

Daly compared this approach to “driving through fog.” When visibility is limited, the prudent move isn’t to stop but to slow down and stay attentive to every sign along the road. This analogy captures the essence of the Federal Reserve’s current stance — cautious, data-driven, and mindful of both risks and opportunities.

Interest Rates: No Rush to Cut

Perhaps the most closely watched topic in Daly’s remarks was the question of future interest rate moves. With inflation gradually easing, investors have been eager for clues about potential rate cuts. However, Daly maintained a cautious tone. She reiterated that any shift toward easing monetary policy must be grounded in clear and consistent evidence that inflation is moving sustainably toward the target.

In her view, current policy remains appropriately restrictive. This restraint, she argued, is not punitive but necessary to restore long-term stability. Daly also suggested that the so-called “neutral rate” — the interest rate that neither stimulates nor slows the economy — may be higher than previously thought. If true, this would mean that even as inflation moderates, rates could remain elevated for longer than markets anticipate.

She was careful not to give a timeline for policy adjustments but stressed that the Fed’s decisions will be based on outcomes, not expectations. “We must let the data lead,” she emphasized. In an environment where both inflation and growth data can surprise, patience and discipline are vital.

Labor Market Dynamics and Broader Economic Health

Another central theme of Daly’s address was the evolving nature of the labor market. The post-pandemic era, she noted, has reshaped work in profound ways. Labor participation has improved, but hiring patterns are shifting, and certain industries continue to face worker shortages. Wages are rising, albeit at a slower pace than in 2022, suggesting that inflationary pressures from the labor market are easing gradually.

However, Daly cautioned against complacency. She pointed out that even as overall employment numbers look healthy, many households continue to feel the strain of higher prices and borrowing costs. Policymakers, she said, must remember that aggregate data can mask uneven impacts across communities. Economic policy should therefore aim not only for national stability but also for broad-based inclusivity.

This human-centered perspective — acknowledging both macroeconomic data and lived experiences — is a hallmark of Daly’s leadership style. She believes that successful policymaking requires empathy and understanding of how decisions affect everyday lives.

Flexibility: The Key to Modern Policymaking

Throughout her speech, Daly returned to the theme of adaptability. The economic landscape, she argued, has entered a new era where traditional assumptions about growth, inflation, and interest rates no longer apply. In such a setting, rigid adherence to old frameworks could prove counterproductive.

Instead, she advocated for a pragmatic, flexible approach that combines rigorous analysis with openness to new ideas. “We must be willing to adjust,” she said, “not because we lack conviction, but because the world is changing.”

This philosophy, she added, does not mean abandoning caution. Rather, it means embracing uncertainty as a constant and building policies that can withstand it. Daly’s vision is one where central banks operate less as rule-followers and more as adaptive problem solvers — capable of navigating complexity with both intellect and intuition.

A Call for Patience and Perspective

In closing, Daly called for patience — both from policymakers and the public. Restoring price stability, she said, is not a sprint but a marathon. The progress made so far is meaningful, but the final mile may be the toughest. What matters most now is staying the course, resisting the temptation to overreact to short-term fluctuations, and maintaining confidence in the process.

Her message resonated with both humility and resolve. Daly’s view of “policymaking amid change” acknowledges that uncertainty is unavoidable but not unmanageable. Through steady hands, flexible thinking, and commitment to the greater good, she believes the Federal Reserve can guide the economy toward lasting stability.

In essence, Mary Daly’s speech offers a masterclass in modern central banking — one that blends data, judgment, and empathy. It reminds us that economic policymaking, at its best, is not just about numbers and models but about understanding people, adapting to change, and leading with both caution and courage.